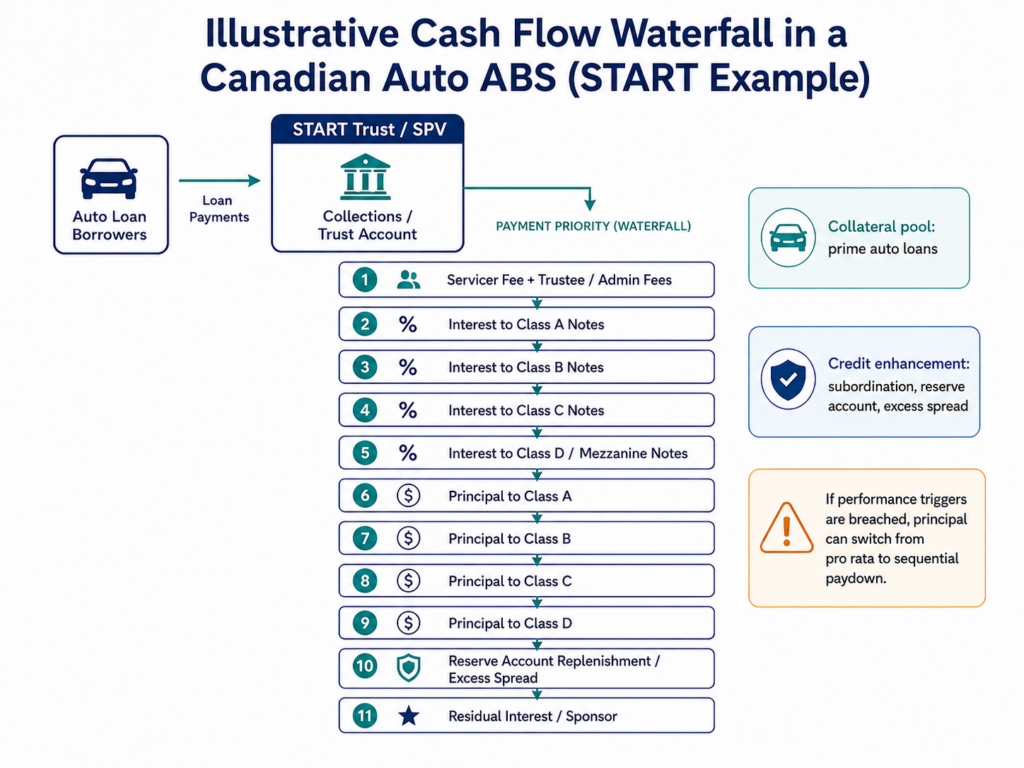

Securitized Term Auto Receivables Trusts (STARTs) are Canadian auto-loan asset-backed securities (ABS) structured as true-sale trusts. In a START, pools of auto loans (the collateral) are transferred into a special-purpose vehicle (SPV) that issues multiple tranches of notes (senior/class A through mezzanine and subordinated classes, often plus a retained residual) to investors. Monthly cash flows from the loan pool (interest and principal payments) are passed to the trust and distributed in priority (the “waterfall”) to pay fees, interest and principal on the notes, with residual cash (excess spread) flowing to the sponsor. STARTs typically feature credit enhancement via subordination (mezzanine tranches, overcollateralization) and a cash reserve, with triggers that can alter payment priority if performance deteriorates.

Scotiabank launched Canada’s START program in 2016. It issued several START transactions (START 2016‑1, 2017‑1, 2017‑2, 2018‑1, 2018‑2, 2019‑1, 2019‑CRT, and, after a pause, 2025‑A, 2025‑B, 2026‑A) collateralized by prime auto loans originated by Scotiabank (Bank of Nova Scotia). Early deals were on the order of C$0.7–1.1 billion (e.g. START 2016‑1 had a C$740 m pool; START 2018‑1 only C$739 m), while recent deals have been much larger (e.g. START 2025‑A pool ~C$2.99 billion, START 2025‑B ~C$2.94 billion). These pools typically contained tens of thousands of loans with weighted‐average remaining terms ~3–4 years (e.g. 2017‑1 W.A. 46 months; 2025‑A W.A. 52 months). Scotiabank (or an affiliate) serves as the servicer, collecting loan payments and handling delinquencies/repossessions, while a trustee (e.g. an institutional trust company) administers the trust. Scotiabank’s investor reports (available on its website) are published monthly, providing detailed static‐pool data and performance metrics for each START trust.

START programs are not unique to Scotiabank; other Canadian banks and finance companies have similar auto-ABS programs. For example, BMO’s Canadian Pacer Auto Receivables Trust (CPART, started in 2018) has issued multiple transactions (e.g. CPART 2018‑1/2018‑2) with similar tranching and monthly reporting. RBC (via its U.S. funding arm under the “Drive Auto Receivables Trust” name) and Ford Credit Canada (with the Ford Auto Securitization Trust) are other active issuers of Canadian auto ABS. The table below compares several programs by sponsor, name, launch year, typical deal size, and structure:

| Issuer (Sponsor) | Program (ABS Issuer) | Launch Year | Typical New Issuance (approx.) | Structure Notes |

|---|---|---|---|---|

| Scotiabank (BNS) | START (Securitized Term Auto Receivables Trust) | 2016 | C$0.7–3.0 b (pool) (~US$500m–2.1b) | Multi‑tranche (Class A–D + Residual), fixed & floating notes; large early amortization; sponsor retains residual (RegRR retention). |

| BMO | CPART (Canadian Pacer Auto Receivables Trust) | 2018 | C$0.4–1.5 b (pool) | Multi‑tranche (Class A–C), fully fixed-rate tranches; sponsor retains overcollateralization as credit enhancement; shorter seasoning. |

| RBC (Santander) | Drive Auto Receivables Trust | ~2020 | US$1–3 b (pool) | U.S.-style Delaware SPV under Reg AB; multiple classes (senior + equity/deferrable); notable for retaining residual equity tranche (varies by deal). |

| Ford Credit Canada | Ford Auto Securitization Trust | 2019 | C$0.4 b (pool) | AAA-rated ~US$325m (C$417m) issuance; prime auto loans; DBRS notes strict collateral criteria. |

Waterfall

Investors receive payments via a cashflow waterfall: fees to the servicer/trustee come first, then interest on the senior bonds, then mezzanine interest, then principal amortization in senior-to-subordinate order, with any excess to the residual holder. In START, there are typically four “A” notes plus B, C, D tranches (all fixed-rate) and the floating-rate RR residual. The waterfall ensures senior noteholders (usually rated AAA) get paid before junior tranches. The diagram below illustrates this priority flow (from top to bottom): fees, Class A interest, Class B–D interest, then principal, with the residual last.

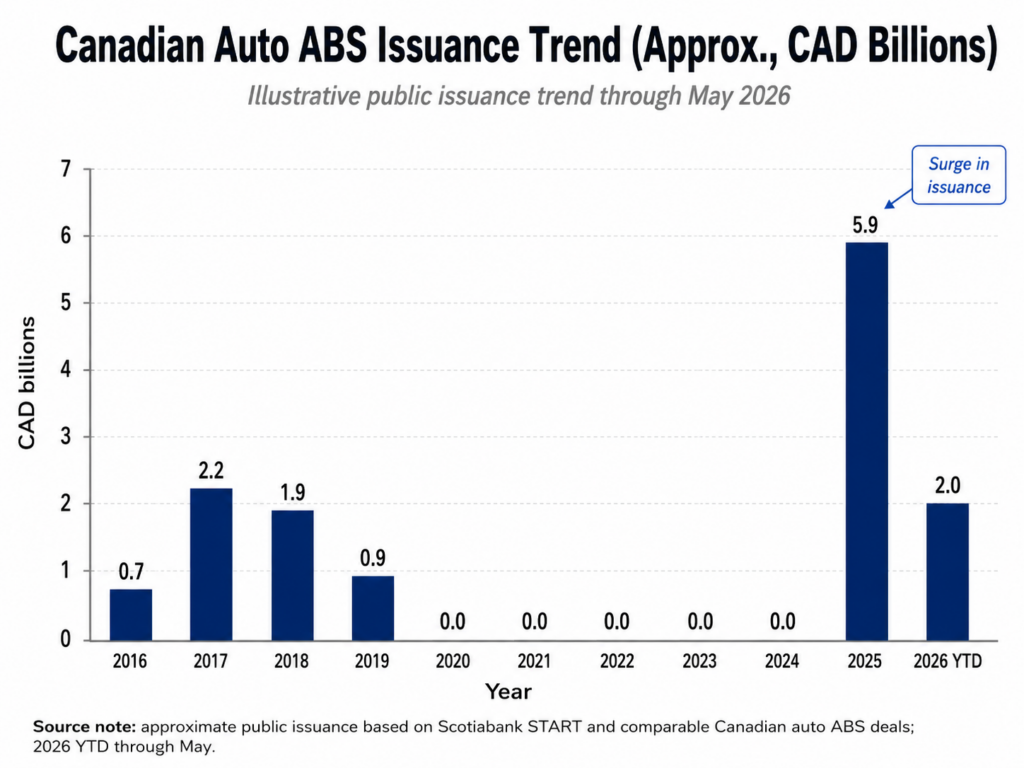

Issuance History and Volume Trends

Scotiabank launched START in 2016. According to Scotiabank’s reports, two START deals were issued by late 2017 (about C$1.5 billion total in notional pool size). Subsequent series (2017-2, 2018-1, 2018-2, 2019-1) were issued through 2019; for instance, START 2019-1 syndicated about $896 million CAD of auto loans in February 2019. No new term auto-ABS were issued from 2020–2024 (a “pause” likely due to market conditions), but START was revived in 2025. In January 2025 START 2025-A closed with ~US$2.105 billion of loans, followed by START 2025-B (~US$2.105 billion in June 2025) – roughly C$3.0 billion each. (By contrast, earlier START pools were ~$0.7–1.0 billion.) New issuance has surged, reflecting rising auto loan demand.

Mechanics: Credit Enhancement and Structure

A START is structured as an SPV (typically a statutory trust) that acquires a pool of car loans from the originator (a true sale). True sale means that legal title to the loans moves to the trust, insulating them from originator bankruptcy. The trust issues amortizing notes in tranches to fund the purchase of the loan pool. In Scotiabank START deals, this has meant senior Class A and mezzanine Classes B, C, (and sometimes D) with staggered maturity dates, plus a residual “RR” tranche often held by Scotiabank to meet U.S. risk-retention rules. Some START transactions (2017‑1, 2018‑2, etc.) split Class A into multiple sub-tranches (A‑1, A‑2, etc.).

The cash-flow waterfall works as follows: loan payments (interest + principal) flow into a trust account monthly. First, servicing and trustee fees are paid. Then interest is paid pro rata to all note classes. Next, principal is paid out. START trusts generally pay principal pro rata to each class up to their target allocation, as long as performance is good. However, if a defined “sequential principal payment trigger” occurs (typically due to rising delinquencies or insufficient interest coverage), then principal is paid sequentially by class (senior to junior). In the normal course, any remaining cash is swept into the overcollateralization/reserve accounts or ultimately to the residual equity holder.

Credit enhancement: START transactions rely on subordination and cash reserves as credit cushions. Initially, the pool size exceeds the sum of senior notes, creating overcollateralization. For instance, START 2016‑1 had an initial pool of C$739.9 m backing only C$699.0 m of Class A–C notes – about 5.7% of the pool was “excess.”

Servicer role: The sponsor (Scotiabank) typically acts as servicer under a servicing agreement. The servicer collects borrower payments, advances funds to the trust if needed, and handles delinquencies/collections. If a loan goes bad, the servicer may repossess and liquidate the vehicle; proceeds (recoveries) go back to the trust pool. .

Payment timing: START distributions to noteholders occur monthly (often on the 25th), funded by the prior month’s collections. The monthly reports show the “Collection Period” and “Distribution Date.” For example, START 2025‑A was issued on 1/30/2025 and had a collection period for Dec 2024/Jan 2025, with distribution on 2/25/2025.

Triggers and events: START indentures include triggers such as interest coverage (liens or “IC” triggers) or delinquency thresholds. When a trigger is hit (e.g. 60+ day delinquencies exceed a set % of pool), the waterfall may “lock up” junior payments or accelerate loss absorption.

Portfolio Performance and Delinquencies

Canadian prime auto loan delinquency remains low by consumer-credit standards. Industry-level 60+ day auto delinquency improved to 0.90% in Q4 2025, while Scotiabank’s START 2026-A pool reported only 0.48% total delinquency and 0.02% cumulative net losses as of the May 2026 collection period. This supports the view that Canadian prime auto ABS continues to demonstrate stable collateral performance.

In summary, Scotiabank’s START program exemplifies Canada’s renewed auto-ABS market. The structure is standard for securitized auto loans: a static pool, with credit support via subordination and sponsor retention. Recent issuance suggests banks value this funding source again. For investors, START and similar auto-ABS can provide stable cash flows and credit enhancement, with relatively low delinquency history. However, one should monitor auto loan delinquencies (especially if economic conditions change), as well as issuer incentives. As always, reviewing the official offering documents and servicer reports is critical for understanding the exact cashflow rules and collateral performance.

Sources: Scotiabank START investor reports and financial filings; TransUnion/industry data; rating agency research on Canadian auto ABS; industry press (e.g. American Banker).

Leave a Reply